Dear investors and well-wishers,

The fund fell 7% in April, but we are up >20% in May so far, taking us to over +40% for the calendar year-to-date.

NVDA

Nvidia reported last night, with revenue up 18% on the quarter and 262% on the year.

There were some shareholder friendly announcements. The stock will split 10:1, dividends will rise 150%, and the company completed a $7.8 billion buyback in the quarter.

Goldman forecasts buybacks will increase from $9.4 billion this financial year to $32 billion in FY25, $60 billion in FY26 and $80 billion in FY27. Large numbers, even by megacap tech standards.

We have discussed our bull case in semis at length: the ~4x increase in capacity planned for the next four years, the $200 billion annual capex plans of hyperscalers (and growing), and the >$200 billion of Government subsidies (also growing). As of today end customer demand is strong. Microsoft is opening a datacenter every three days, and once live, these are operating at full capacity in 3-5 hours.

This investment, much of which lands directly on Nvidia's income statement, is driven by return on capital.

Jensen Huang shared some detail on the call.

For every $1 spent on NVIDIA infrastructure, at current pricing, cloud providers will earn $5 over the following four years, which aligns with our channel checks suggesting hyperscalers recoup spend on NVIDIA chips in less than 12 months. It's easy to spend up when your first-year return is over 100%.

One of our concerns is that the most advanced chips are becoming obsolete too quickly. But at these returns, that's certainly less of a problem.

Additionally, we learned every $1 spent on NVIDIA's HGX H200 servers can generate $7 over the next four years, again with the caveat that this is calculated at current pricing, which will certainly change.

This is what's driving NVIDIA's results: lavish returns to the companies buying their products.

So if NVIDIA's winning, who's losing?

We learned last night that Snowflake is downgrading profit forecasts 'in light of increased GPU-related costs related to our AI initiatives”

So this fits with our thesis outlined in our last letter, where NVIDIA becomes a cost that many other companies have to pay, the same way that Microsoft taxes nearly every white collar worker, and Google and Facebook harvest data from every user on the internet, and then extract the highest quality revenue from nearly every online business.

There's a precedent for a megacap tech company becoming both critical to its users, while also extracting substantial value from them. There will likely be more losers than winners here.

We have a clear profit target and a clear risk management framework so when the boom does turn to bust, if say, the hyperscalers don't get the returns they're expecting and scale back their plans, and/or Government incentives swamp the market with supply, we have clear levels at which we will move to cash.

At the moment though, it seems more likely that our semiconductor positions will hit their 4x profit targets.

Fortunately, we are long the leaders. I'm unsure who originally made this image but will credit if I find out.

Reporting season

This week marked the end of reporting season for us.

It was a bit of a bloodbath in midcap tech, which we managed to dodge this time.

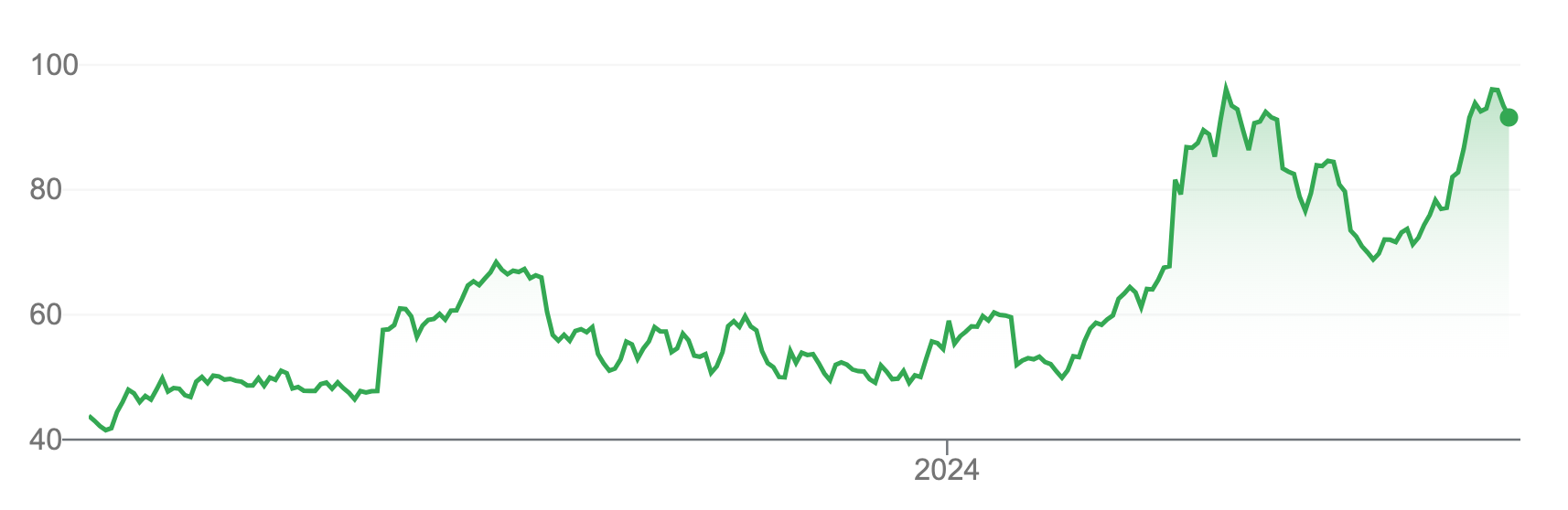

Crowd favourites (which we don't currently own) like Shopify, Square and Twilio are still languishing. The problem is these are still very large companies making very little money.

Shopify

Shopify has a $74 billion market cap but reported only 23% revenue growth and an operating profit of just $86 million for the quarter (and a GAAP loss of $281 million). That is a big valuation for what we consider low growth and basically no profits.

Twilio

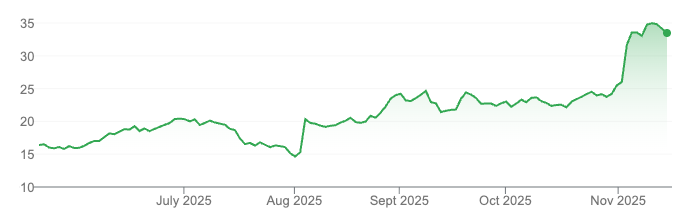

Twilio reported 7% growth and a quarterly loss of $55 million, which admittedly is an improvement on last year (-$342 million), but the company is still somehow trading at a market cap of $10 billion. The increasing share count mutes any prospects of a recovery.

I've shared this before, but it was over a year ago now that Twilio reported the CEO was paying his direct reports A$50 million each per year. I'm sure everyone in the office finds his jokes hilarious. The CEO bought the Onion and then asked on twitter for readers to chip in a dollar each. Surely he can't have run out?

Source: Twilio 2022 report, still impressive two years later

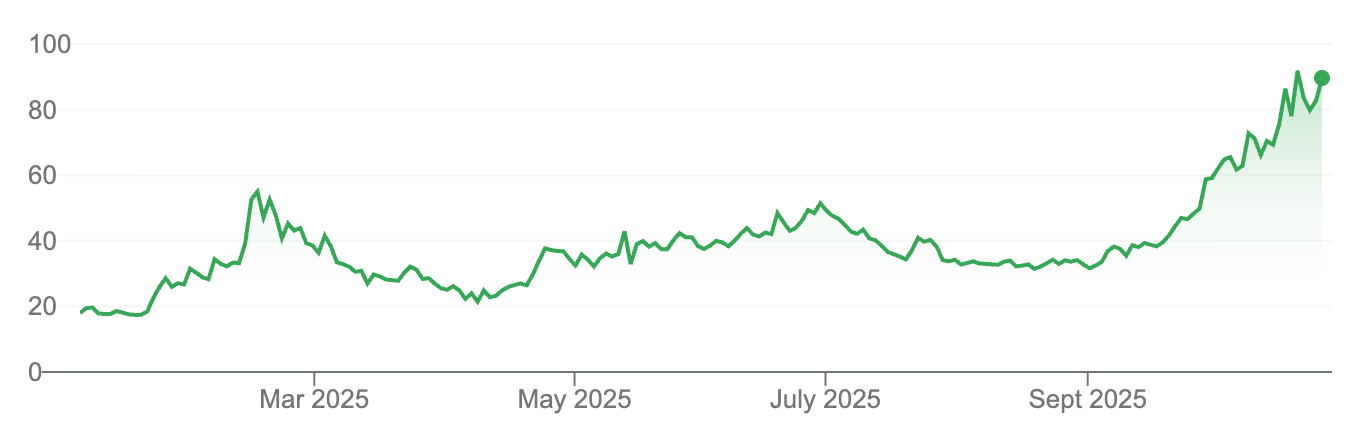

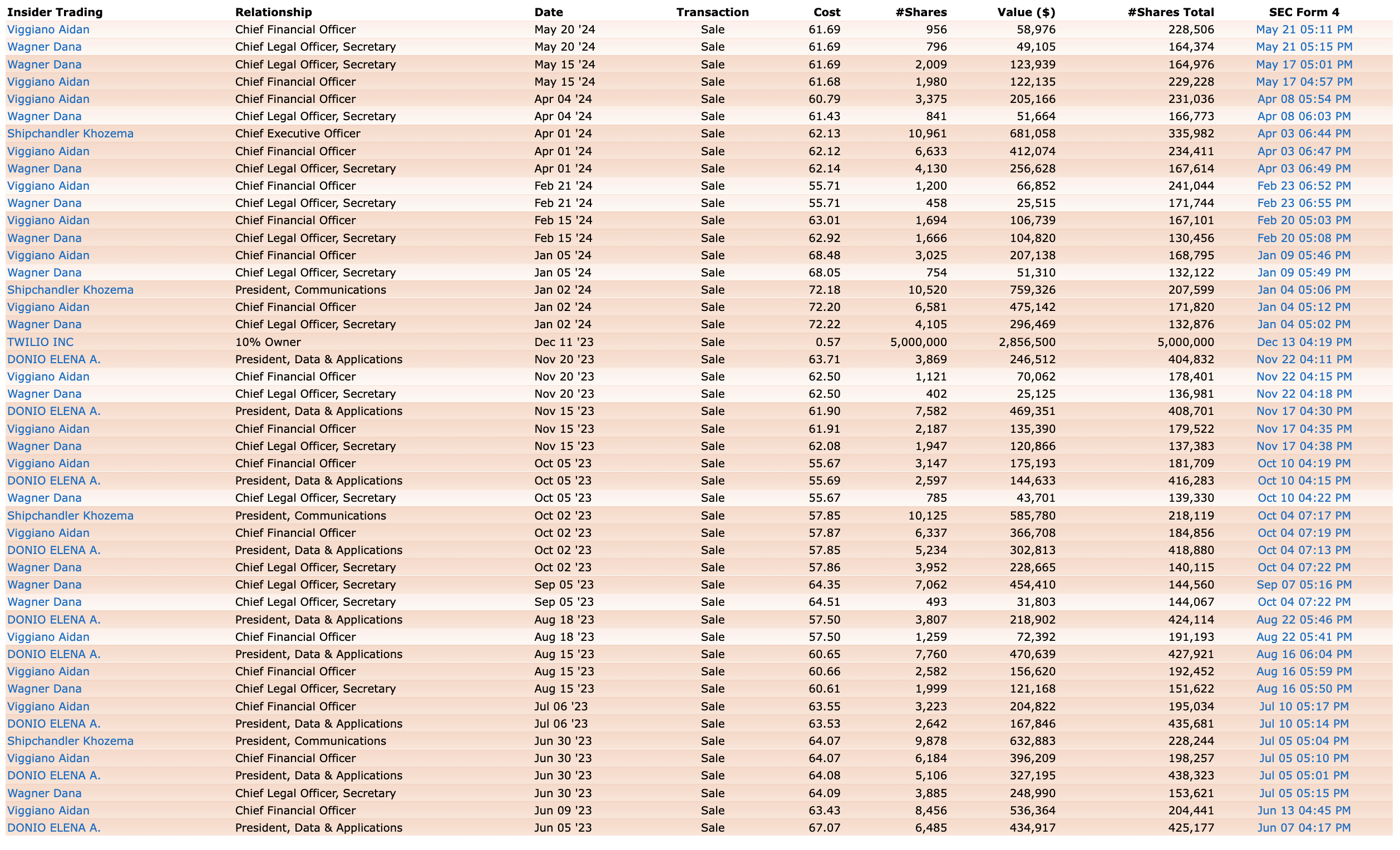

If you buy the stock, you could well be buying off insiders earning tens of millions a year, who have themselves chosen to sell.

Twilio insider buys and sells, but only sells in this case

Anyway, enough about stocks we don't own. We had a lucky reporting season with our major positions holding up. To give a quick run down in order of decreasing size:

Transmedics

Transmedics reported revenue growth of 133%, a 19% increase on the prior quarter alone, and more importantly a 13% GAAP after-tax profit margin.

The hair-raising sell-off late last year came on the back of a surprise decision to buy aircraft. It seems that bet is paying off.

Transmedics now has 14 operational planes, and should reach 20 by the end of this year. They are doing ~50% of missions on their own aircraft, which allows them to capture margin that would have otherwise gone to aircraft operators and brokers, while making the entire process more efficient.

They are accumulating more and more data that their organs-in-a-box, partly developed at St Vincent's in Australia, offer better health outcomes (rather than just non-inferiority) than the prior standard: a bucket of ice.

Clarity Pharmaceuticals

Clarity rallied after an impressive patient update which we discussed in a prior letter.

Johnson & Johnson reported last night that four patients died in an early trial of Actinium-232, an alpha particle, behind more than one recent multi-billion dollar acquisitions.

The hope was that alpha particles, with a shorter range and greater destructive power, could work better in radiopharmaceuticals.

Perhaps this study casts a chill on this line of investigation, and returns attention to beta-emitters, like the copper isotopes used by Clarity.

Acquisitions in the US have been at several times Clarity's current market value (~US$800 million).

It's worth remembering why there is so much big pharma interest in the space. Prostate cancer is often curable, but the side effects are horrific. After rounds of invasive biopsies, prostate removal, hormone therapy, and chemotherapy, men are often impotent, incontinent, or both. Certainly miserable.

Radiotherapies are more targeted and have much milder side effects (it messes with salivary glands, for example), and we are on the side of experts who expect it to move to front-line treatment, one way or another.

Nubank

Nubank reported revenues up 64%, revenue-per-customer up 30%, and net profits up 159%. The company crossed 100 million customers, and is growing faster in Mexico than it was in Brazil at a similar stage.

So the thesis of growing customers, growing revenue-per-customer, and successful entry into new countries in South America is on track.

Celsius

Celsius reported 60% (adjusted) revenue growth, and the stock recovered from a plunge in April.

Celsius is in the early stages of an international roll-out across the UK, the EU, Canada, and we are assured, Australia.

You might have to try it to understand why it has taken so much market share from Red Bull and Monster. I would never drink a Red Bull and try and avoid even looking at cans of Monster, but I found orange Celsius addictive.

MercadoLibre reported solid results, Sea Ltd is back on the path to profitability, and has steadied its market share vs Tik Tok, which was a bit of a wild card and quickly took ~15% of e-commerce in the region. This is one of the last stocks we own from the boom/bust period but it does finally look back on track.

Finally, I recorded an interview with Tom Buckley and Dexter where they asked some new questions.

Best wishes

Michael

Interview with Tom Buckley and Dexter Eugenio

Disclaimer

The information in this note has been prepared and issued by Frazis Capital Partners Pty Ltd ABN 16 625 521 986 as a corporate authorised representative (CAR No. 1263393) of Frazis Capital Management Pty Ltd ABN 91 638 965 910 AFSL 521445. The Frazis Fund is open to wholesale investors only, as defined in the Corporations Act 2001 (Cth). The Company is not authorised to provide financial product advice to retail clients and information provided does not constitute financial product advice to retail clients.

The information provided is for general information purposes only, and does not take into account the personal circumstances or needs of investors. The Company and its directors or employees or associates will use their endeavours to ensure that the information is accurate as at the time of its publication. Notwithstanding this, the Company excludes any representation or warranty as to the accuracy, reliability, or completeness of the information contained on the company website and published documents.

The past results of the Company’s investment strategy do not necessarily guarantee the future performance or profitability of any investment strategies devised or suggested by the Company.

The Company, and its directors or employees or associates, do not guarantee the performance of any financial product or investment decision made in reliance of any material in this document. The Company does not accept any loss or liability which may be suffered by a reader of this document.