Dear investors and well-wishers,

The fund returned 32% in May, which combined with a >10% move so far in June, has taken us to +80% for the calendar year-to-date.

We’ve been helped by owning the best-performing stock on the S&P500, Nvidia, and some of the top performers on the ASX, like Clarity Pharmaceuticals and Droneshield, which is already up more than 2x from our first recent purchases.

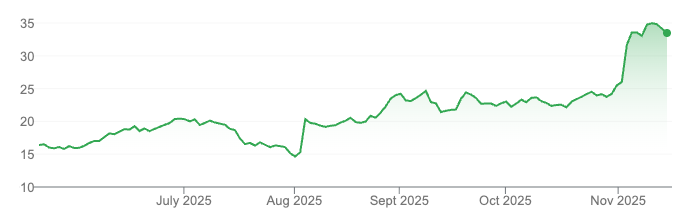

Droneshield

We’ve had moves like this before, but this is the first time in relatively lacklustre markets.

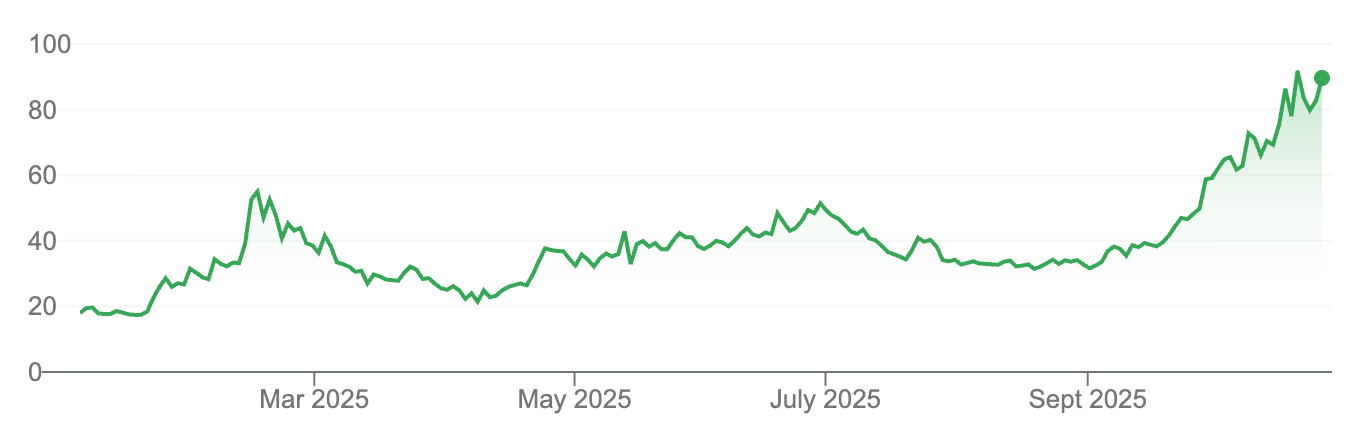

Clarity Pharmaceuticals

Clarity had a large move in May and is now largest position, followed by Transmedics, which we reduced by a third. (Our price target was set at a 2.5x profit, but we decided that 2.25x was close enough in the context of a large move across the portfolio to start cashing in).

Transmedics

Nvidia continued to fire, and we closed the entire position last week.

Towards the end of last year, Nvidia’s multiple was cheap on an absolute and historic basis, especially at »100% organic growth.

Interesting to see $NVDA approaching a 5 year (forward) PE low

Could be +50% next year on multiple alone

8:23 AM • Dec 8, 2023

26 Likes 4 Retweets

5 Replies

After a >150% rally this year, we are now at the opposite end of that range:

Nvidia has moved from the bottom of its recent range to the top. Combined with growth this has generated a 175% return this year.

If you’ve been reading these notes you’ll know how bullish we’ve been on semiconductors, with Nvidia our top pick. We set extremely optimistic profit targets across our semiconductor exposure, and these were hit in the recent surge.

I am sure we’ll get another entry point - perhaps quite soon - and will go again. If you applied this approach systematically to Nvidia over the last 25 years, covering the dotcom crash, 2008-2009, COVID, 2022, and multiple 65-90% drawdowns, you earned nearly 3x the return of the stock itself (1500x vs 500x), with substantially lower drawdowns (53% vs 90%).

This approach has proven surprisingly powerful for our kinds of companies.

An (amusing) example is Carvana, which put us through the ringer in both directions. We first bought at $36, and rode it up nearly 10-fold, after which it collapsed, and has since made a partial recovery.

Carvana stock price

Under immense financial pressure and a heavy debt burden, the company managed to improve their gross-profit-per-unit, close creative financing deals, and kept the company alive. Over the last year or so the stock rallied, and short sellers have had to close one by one.

A remarkable increase in Carvana’s Gross Profit per Unit

Now management is selling again - right into the forced buying of their harshest critics, who are basically transferring cash directly into management’s accounts.

I shared a chart a while ago which showed our risk framework would have captured the bulk of Carvana’s returns, and saved us grief during 2022:

But it’s fascinating to see that it gave a buy signal at almost the perfect time as well:

A risk-focused approach on Carvana would have generated a 25x return

I doubt there’s anyone on the planet that traded this stock this well.

This saved us from temptation in software this year, which has languished with negative returns while a small number of companies in other sectors have driven the market forward.

Software has looked primed for a full recovery multiple times over the last two years, but every time earnings season comes around, leading companies have posted tepid growth, dramatic dilution, and ugly GAAP financials. And would be supporters like us find the compensation plans tough to swallow.

Software focused funds have had a tough time of it and are unlikely to be taking in new money in the near term.

Given these companies are mostly stock issuers, rather than buyers, a recovery will require generalists and outsiders to get interested, which will take GAAP profits and unadjusted economic value creation. Too many of these companies are a long way from that. Presumably at some point that will change, but it hasn’t yet.

Even in this sector, our framework of explosive growth, customer love and true winners still identified the best performing stocks of the bunch. One of the few software companies to break out was Crowdstrike, which maintained high growth, increased GAAP margins, and is raved about by security folk.

Crowdstrike escapes

Summary

Our approach has often identified the highest returning stocks on the ASX and S&P500, and it’s good to see the process working so well again in 2024. But looking back over the last twelve years, there were two issues that occasionally tripped us up.

First, stocks often moved long before fundamentals changed. In early 2022 for example, many companies that later imploded were still reporting strong results. But the damage was done to share prices long before that.

The second issue is that often our companies are wildly exciting, their customers rave about them, they can sell out entire product lines in advance, and double in size year-on-year.

This attracts waves of market attention, whether it’s Nvidia or what ultimately became a circus around Carvana.

This is a strength as well as a weakness, as we’ve never had to have that value investor issue of waiting around for years for the market to see what we see.

We’re keeping our original approach, which once again identified a number of the highest returning stocks in Australia and the United States (and we only hold about 20).

But are adding a disciplined systematic, quantitative approach to harvesting the profits in these speculative surges, while moving to cash when risk signals flash red.

Both sides of this coin were in action this month. For example, we closed Celsius for a modest profit after a drop in market share triggered a sell-off, and we harvested a serious rally in semiconductors from only November last year.

This has already improved our returns, has put us way ahead of market indices this year, while also leaving us with the largest cash balance we’ve had in quite some time. It’s also quite fun, and calming to know exactly where we will move to cash on every position.

We have a long way to go, but will stick to this approach with discipline, sell aggressively when we need to, and make sure we keep finding the next set of top market performers.

Best regards

Michael

ps I have moved our mailing list to a new provider, so please let me know if there are any issues.

If you'd like to invest with us, you can access our investment portal and fund documentation through the button above.

Or simply reply to this email and we'll be in touch.

Disclaimer

The information in this note has been prepared and issued by Frazis Capital Partners Pty Ltd ABN 16 625 521 986 as a corporate authorised representative (CAR No. 1263393) of Frazis Capital Management Pty Ltd ABN 91 638 965 910 AFSL 521445. The Frazis Fund is open to wholesale investors only, as defined in the Corporations Act 2001 (Cth). The Company is not authorised to provide financial product advice to retail clients and information provided does not constitute financial product advice to retail clients.

The information provided is for general information purposes only, and does not take into account the personal circumstances or needs of investors. The Company and its directors or employees or associates will use their endeavours to ensure that the information is accurate as at the time of its publication. Notwithstanding this, the Company excludes any representation or warranty as to the accuracy, reliability, or completeness of the information contained on the company website and published documents.

The past results of the Company’s investment strategy do not necessarily guarantee the future performance or profitability of any investment strategies devised or suggested by the Company.

The Company, and its directors or employees or associates, do not guarantee the performance of any financial product or investment decision made in reliance of any material in this document. The Company does not accept any loss or liability which may be suffered by a reader of this document.